Understanding the New 2018 Federal Income Tax Brackets and Rates

February 8, 2018 by Gordon Advisors

The Tax Cuts and Jobs Act recently passed by Congress and signed by the president includes new tax brackets and rate changes affecting most Americans. Some of the changes are temporary — primarily individual and estate tax changes — and will expire after 2025. Changes to corporate taxation do not have an expiration date.

Here is a simplified look at individual tax brackets, rate changes, and deductions/credits to help you get a better understanding of how the new law affects you, your family and your finances.

Individual income tax changes

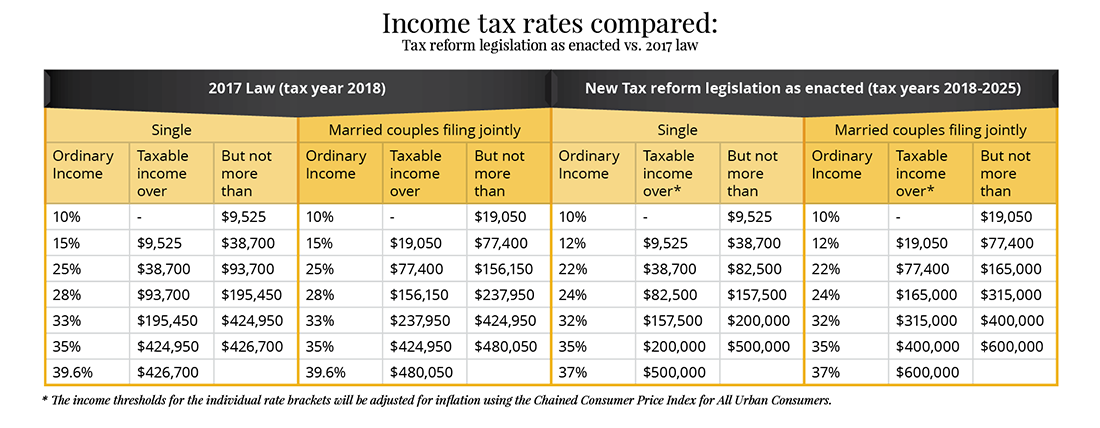

The new individual income tax brackets retained the seven levels of earlier years, but otherwise have changed considerably. First are the substantial standard deduction changes, which for most people means that itemizing deductions to save on taxes is no longer going to be worthwhile. The standard deduction increases are $12,000 for single taxpayers and $24,000 for married taxpayers filing jointly.

Going forward through 2025, the lowest tax bracket, up to $9,525 ($19,050 joint filers), is still taxed at 10 percent but all the remaining brackets are new. Tax payers in the highest tax bracket — single filers with taxable income over $500,000 — dropped from 39.6 percent to 37 percent. For married filing jointly taxpayers, the 37 percent rate applies to taxable income over $600.00, amounting to a “marriage penalty.” See the table below to estimate the changes to your tax bracket.

To deduct or not to deduct

If you accumulate deductions that exceed the amount of the applicable standard deduction, you will want to discuss your options with your tax accountant. Keep in mind, however, that the new law makes several changes to deductions from the past, all of which may affect an average tax payer. These include:

- The mortgage interest deduction is now limited to interest on $750,000 ($375,000 for married filing separate taxpayers) of acquisition indebtedness on primary and secondary residences. Mortgages in existence on or before December 15, 2017 are grandfathered and thus retain the $1 million threshold. Exceptions include binding contracts to purchase property before December 15, 2017.

- The interest deduction for home equity debt is repealed.

- Unreimbursed medical and dental expenses are deductible when they exceed 7.5 percent of adjusted gross income (AGI) in 2017 and 2018, and 10 percent in 2019.

- Miscellaneous deductions not listed in section 67(b) are eliminated.

- Only personal casualty losses that occurred in federally declared disaster areas are now deductible.

- State and local income, sales or property tax deductions are limited. In Michigan, the legislature is working to minimize the impact, although as of this date, no changes have been enacted.

- The AGI limit for charitable donations is up from 50 percent to 60 percent.

- The deduction for making a contribution in exchange for athletic event seats is eliminated.

- The Pease limitation on itemized deductions is repealed.

- The deduction for moving expenses is repealed, except those pertaining to ordered moves by members of the armed forces.

- Alimony payments are not taxable to the recipient and cannot be deducted by the payer.

Credits and the status quo

For those with children, the new law increases the child tax credit (CTC), doubling it to $2,000 for each qualifying child, with $1,400 of that amount (per qualifying child) refundable. The earned income threshold for the refund is now lowered to $2,500 and the income level that triggers the beginning phase out of the credit was also raised to $200,000 ($400,000 for joint filers).

For CTC purposes, the definition of “qualifying child” generally means that the child must be related to the taxpayer (i.e., son, daughter, grandchild, etc.), the child must live more than six months of the year in the taxpayer’s home, and the child cannot provide more than half of his or her own support. Due diligence is required to comply with these rules and divorced or legally separated parents should seek the advice of their tax accountant as special rules may apply.

A few tax rules that did not change include:

- The 20 percent special tax rate for long-term capital gains and qualified dividend income.

- The 3.8 percent tax rate on some net investment income.

- The 0.9 percent FICA-HI tax rate on some earned income in effect under prior law.

- The additional standard deduction for the blind and elderly.

- Contributions to qualified retirement savings plan (i.e., a 401(k) or IRA).

- The dependent care credit.

- The adoption credit.

- The exclusion from gross income of up to $5,000 annually for employer -provided dependent care assistance.

Even a simplification of the new tax law is complicated, so never hesitate to connect with your professional tax advisor with questions or concerns. The tax professionals at Gordon Advisors are among the most informed and are available to assist. Contact us today to get the peace of mind you need.